Stable Isn't the Same as Growth — The Honest Read on the Okanagan Right Now

But it is right where we need to be. You can't build a healthy market on a shaky foundation. Most weekly market updates from realtors are written to make the market sound great honestly you can spin stats for any narrative you want. This isn't going to be one of those.

Here's what's actually happening in the Okanagan right now, why we're trending differently than the rest of BC, and what it means for you.

Where this whole post starts

BCREA — the provincial association for BC realtors — just released their April 2026 housing forecast. View Here. It's the most credible read on the BC market we've got. And it tells a story most of BC is dealing with that the Okanagan isn't.

Three years of shocks got us here. Rates. Tariffs. War. Inflation. Confidence is gone.

2026 doesn't look much better. Sales down another 2.1%. Prices down 1.4%. Third year in a row of slow growth.

2027 is where the recovery shows up. Sales up 7.7%. Prices up 2.9%. But not until next year.

That's the BC story.

Here's the Okanagan story.

We grew when most of BC fell. Sales up 8.7% in 2025. Prices up 2.9%. Greater Vancouver dropped 10.2%. Fraser Valley dropped 16.6%.

For 2026, BCREA's forecasting us flat-to-positive. Sales up 0.3%. Prices up 1.2%. Most of the rest of BC is forecast to fall another 4 to 6%.

We didn't fall the way they did. We're not forecast to fall the way they are.

There's three reasons for that.

Reason one — our owners aren't stressed

41.3% of Kelowna homeowners are mortgage-free. That's about 25,225 households out of 61,020 with zero mortgage payment. Kelowna ranks 8th in Canada.

Here's how that stacks up against other markets:

- Thunder Bay, ON — 47.0% (#1 in Canada)

- Victoria, BC — 43.2% (highest in BC)

- Nanaimo, BC — 42.0%

- Kelowna, BC — 41.3%

- Vancouver, BC — 40.8%

- Kamloops, BC — 40.0%

- Chilliwack, BC — 38.0%

- Abbotsford-Mission, BC — 34.0%

- Milton, ON — 21.0% (most-mortgaged in Canada)

The pattern is clear. BC's older, established markets cluster at the top. Newer commuter markets sit much lower. We're closer to Victoria and Vancouver than we are to the Fraser Valley when it comes to owner stability.

When owners aren't getting squeezed by renewals or rate hikes, you don't see forced selling. They sell when they want to. Not when they have to. That's a structural difference and it matters.

Reason two — the economy is diversified

YLW pushed 2.3 million passengers through in 2025, up 8.5%. That generates around $2 billion in regional economic impact. Building permits hit $1.35 billion in 2025, up from $1.14 billion in 2024. 17,299 licensed businesses in the region. 750 manufacturing firms in the Okanagan Manufacturing Database.

Three different economic engines across the valley.

Kelowna runs on services, healthcare, tech, and tourism. Q3 2025 unemployment was 4.9% — lower than BC (6.17%) and Canada (7.03%) at that point. Top job-posting sectors: retail, accommodation/food, healthcare.

Vernon runs on manufacturing, retail, and construction. Employment rate of 58.7% — ranks 11th out of 94 BC small areas. Anchor of the North Okanagan, serving a regional population of more than 100,000.

Penticton's industrial sector quietly does $800 million to $1 billion a year in economic impact, with about $500 million in direct outside-the-region sales. That dwarfs tourism. About 15 manufacturers in the central industrial area, several with 50+ employees each.

We're not a one-industry town. When something slows, something else picks up.

Reason three — the buyer pool is different

Our buyers are equity-rich, lifestyle-driven, and a lot of them are coming from the Lower Mainland or Alberta. Less leveraged. Less rate-sensitive. Less likely to panic.

The price gap matters here. Vancouver detached is averaging $2.09M. Okanagan detached is averaging $984K. That's a 53% discount on a single family home if you're moving here from Vancouver. The lifestyle math has been there for years. The financial math is now there too.

The 10-year picture

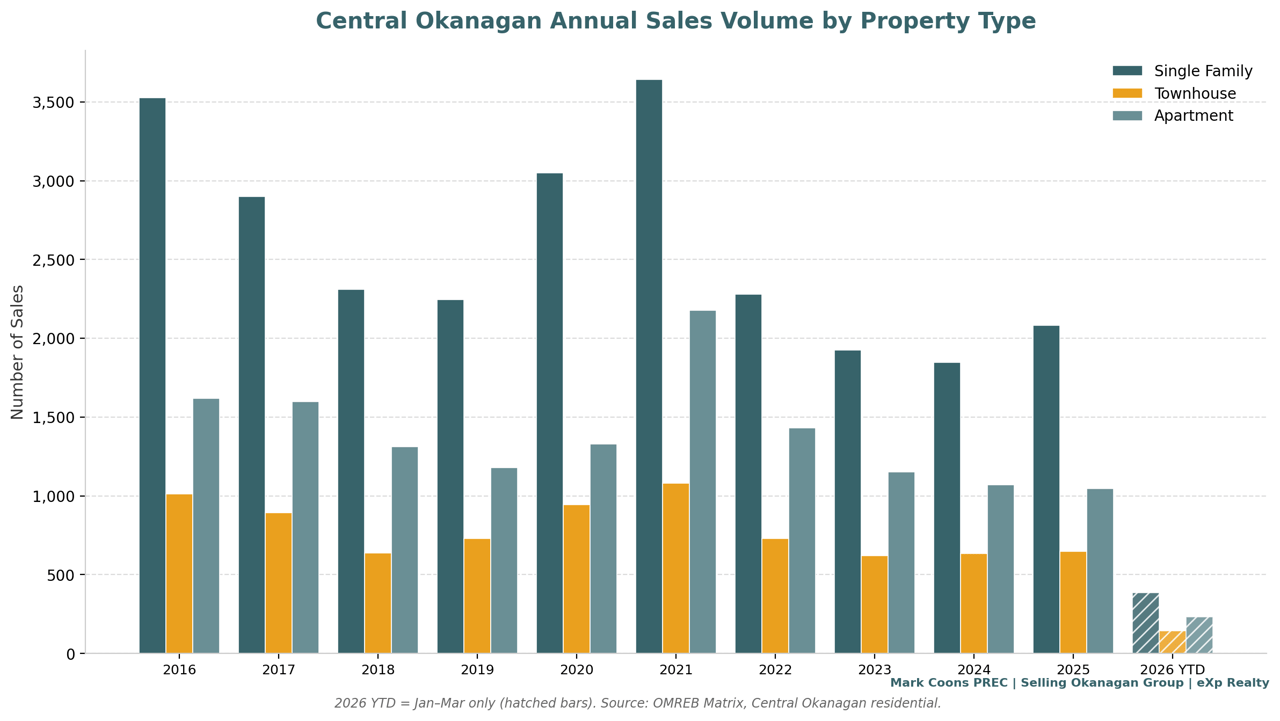

I pulled the last 10 years of Central Okanagan sales out of Matrix. Here's what the trend actually looks like through Q1 2026.

Volumes peaked in 2021. Bottomed in 2023 and 2024. Stabilizing now. Single family was the only segment to post a real recovery bounce in 2025 — up 13% over 2024.

Here's the full annual breakdown:

| Year | Single Family | Townhouse | Apartment |

|---|---|---|---|

| 2016 | 3,527 | 1,013 | 1,619 |

| 2017 | 2,901 | 893 | 1,599 |

| 2018 | 2,309 | 637 | 1,313 |

| 2019 | 2,247 | 731 | 1,181 |

| 2020 | 3,048 | 944 | 1,328 |

| 2021 | 3,643 | 1,079 | 2,178 |

| 2022 | 2,279 | 730 | 1,430 |

| 2023 | 1,924 | 620 | 1,153 |

| 2024 | 1,847 | 634 | 1,070 |

| 2025 | 2,083 | 648 | 1,047 |

| 2026 YTD (Jan–Mar) | 384 | 143 | 233 |

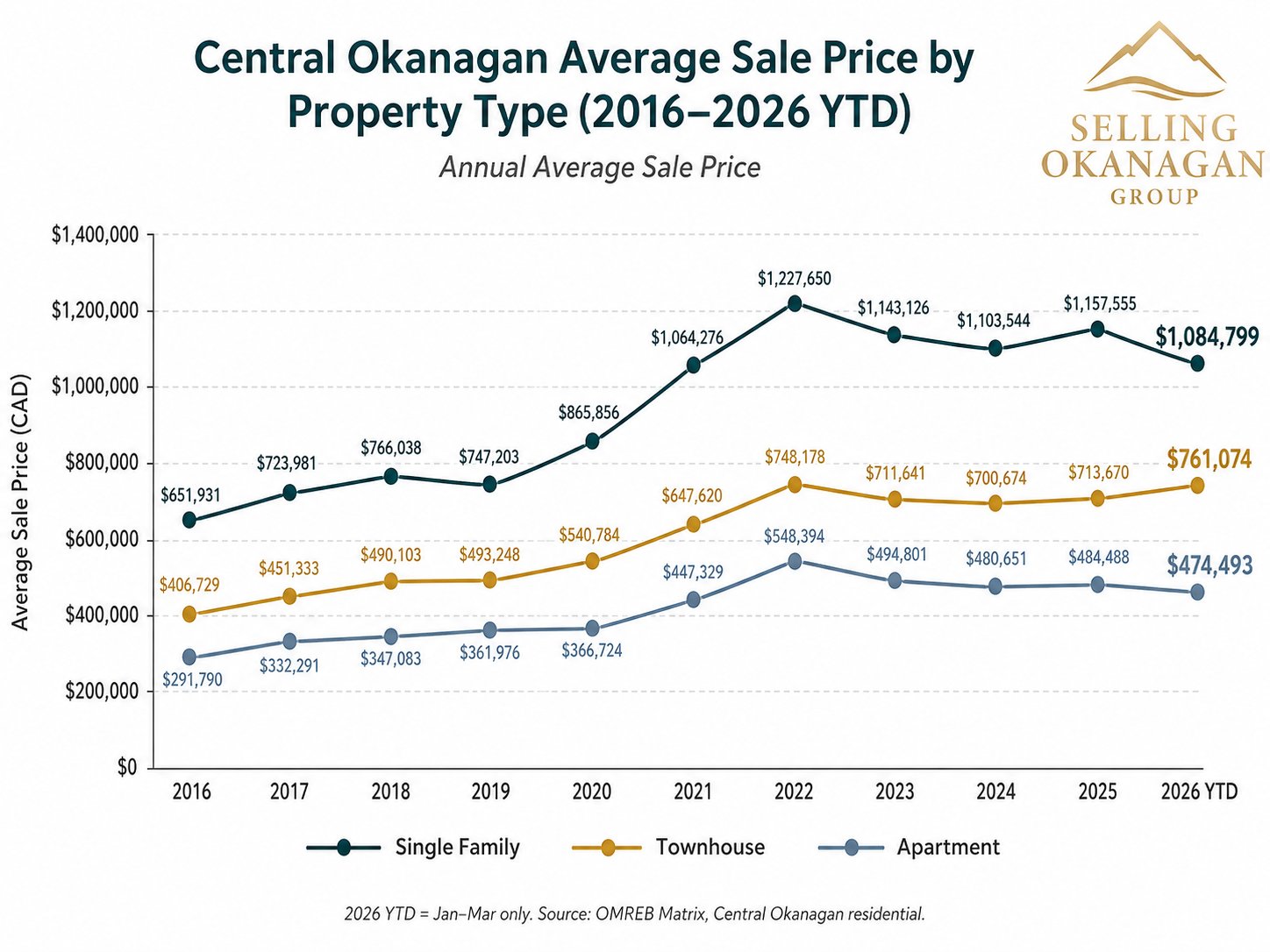

Two things worth flagging on prices.

Single family peaked in 2022 at $1.23M and still hasn't gotten back there. 2026 YTD is sitting at $1.08M. So we're still working off the peak.

But townhouse just hit a new 10-year high at $761K. That beats the 2022 peak of $748K. It's the only segment to do it. That's not a number anybody is talking about and it should be.

Annual price breakdown:

| Year | Single Family | Townhouse | Apartment |

|---|---|---|---|

| 2016 | $651,931 | $406,729 | $291,790 |

| 2017 | $723,981 | $451,333 | $332,291 |

| 2018 | $766,038 | $490,103 | $347,083 |

| 2019 | $747,203 | $493,248 | $361,976 |

| 2020 | $865,856 | $540,784 | $366,724 |

| 2021 | $1,064,276 | $647,620 | $447,329 |

| 2022 | $1,227,650 | $748,178 | $548,394 |

| 2023 | $1,143,126 | $711,641 | $494,801 |

| 2024 | $1,103,544 | $700,674 | $480,651 |

| 2025 | $1,157,555 | $713,670 | $484,488 |

| 2026 YTD | $1,084,799 | $761,074 | $474,493 |

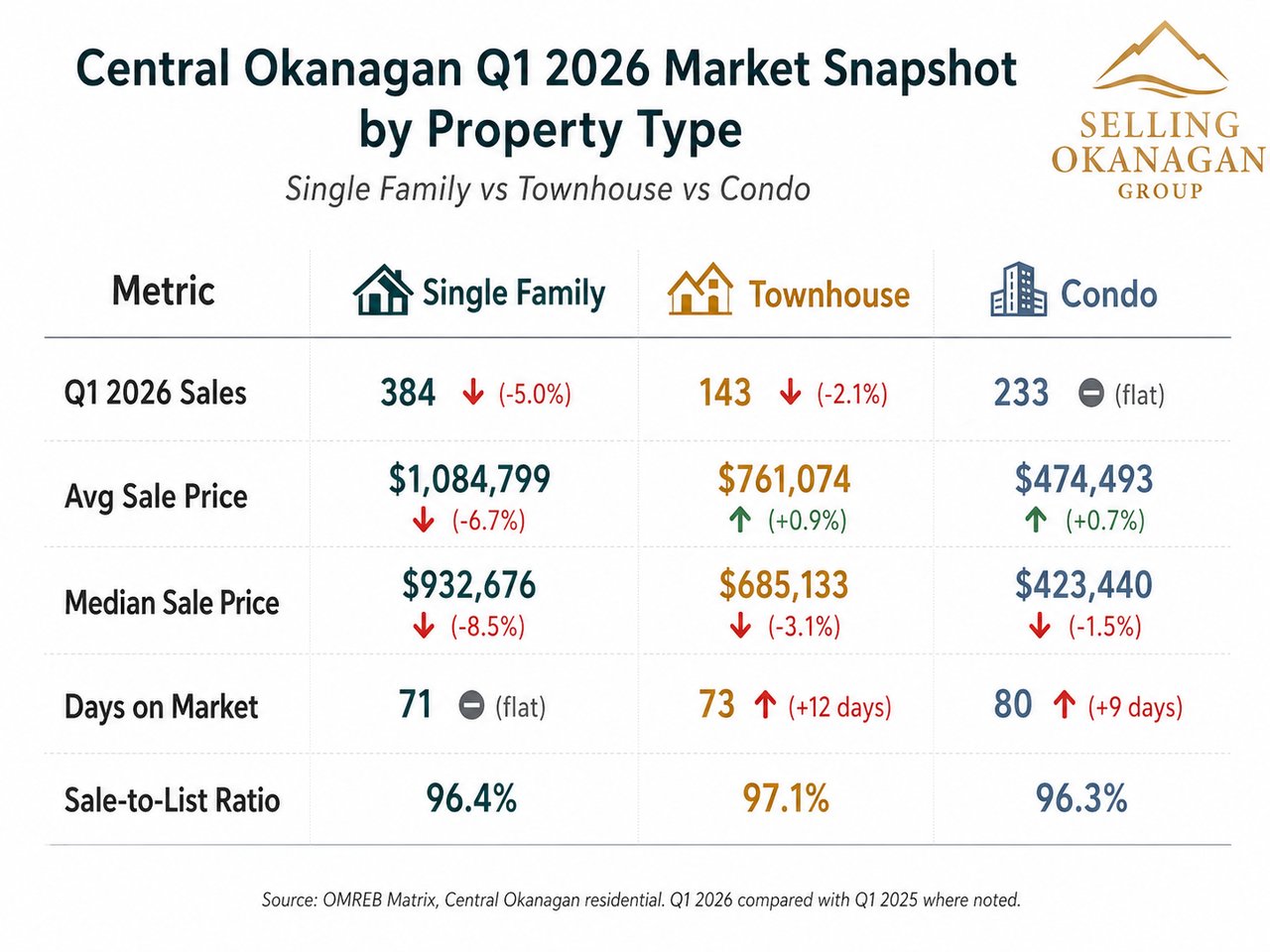

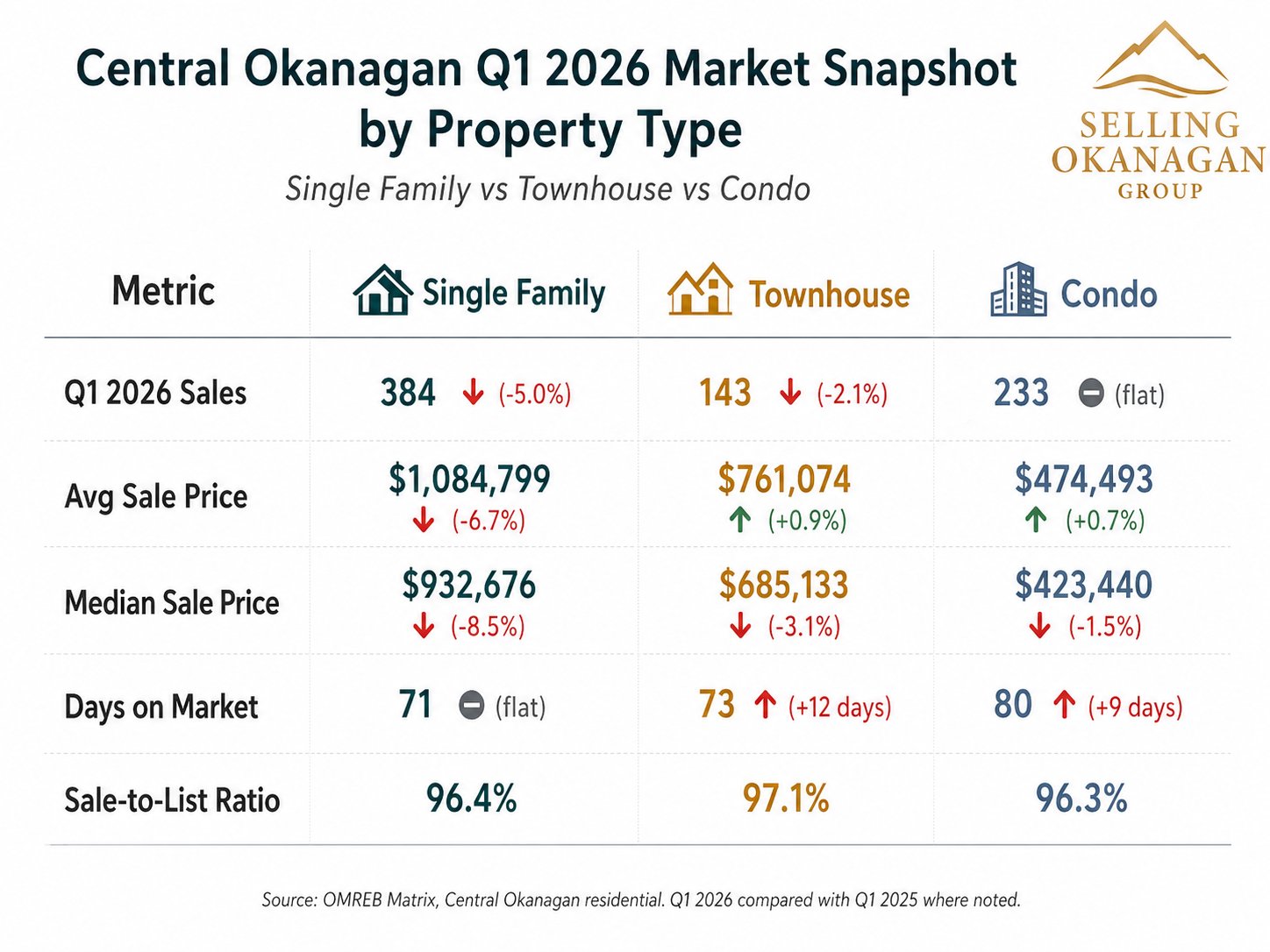

Q1 2026 — the honest update

Here's how Q1 2026 stacks up against Q1 2025.

The detail:

| Metric | Single Family | Townhouse | Condo |

|---|---|---|---|

| Q1 2026 sales | 384 (-5.0%) | 143 (-2.1%) | 233 (flat) |

| Avg sale price | $1,084,799 (-6.7%) | $761,074 (+0.9%) | $474,493 (+0.7%) |

| Median sale price | $932,676 (-8.5%) | $685,133 (-3.1%) | $423,440 (-1.5%) |

| Days on market | 71 (flat) | 73 (+12 days) | 80 (+9 days) |

| Sale-to-list ratio | 96.4% | 97.1% | 96.3% |

Single family is the soft spot in Q1. The average dropped 6.7% but the median dropped 8.5%. That tells me fewer high-end transactions are closing — not that the mid-market is dropping by 7%. Different problem with a different solution.

Townhouse and condo volumes are basically flat. But days on market is stretching out. Buyers are taking longer to pull the trigger. Sale-to-list ratios at 96-97% confirm what the days on market is showing — sellers are negotiating 3 to 4% off list. Not getting bid up.

The condo and STR shift

Last week I wrote about the 16 STR-exempt buildings and what's about to happen on June 1. Quick recap — the City of Kelowna's opt-out from the provincial principal residence rule means those 16 buildings can keep operating short-term rentals as a principal use. First exemption of its kind anywhere in BC.

The condo segment got hit hardest by the combination of rate increases, broken investor math, and STR policy uncertainty. That's been true for almost two years.

But the picture is changing. With the June 1 opt-out confirmed, the legal STR-zoned buildings have a clearer runway than they've had since 2023. The investors who walked away in 2024 are starting to look again.

What that means for the broader condo market: as those 16 buildings get absorbed, the condo segment as a whole tightens up. Some of that demand starts spilling into other Kelowna inventory.

The supply of STR-eligible buildings is permanently capped at 16. That's the regulatory moat. It's not going to expand. What gets bought in this window is what's available — likely for a long time.

Too early to call it a full recovery. But the leading indicators are pointing the right way for the first time in two years.

What's not great — and I'm not going to pretend it is

- Q1 2026 sales are down across the board versus Q1 2025

- Unemployment hit 11% in Kelowna in November 2025 (highest in Canada at one point) and finished the year at 8.6%

- Population estimate for 2026 was downgraded from 261,000 to 247,000. People are leaving, mostly to Alberta for jobs and cheaper housing

- Active listings are near a decade-high. Sellers have more competition than they've had in years

- Housing starts dropped to 2,600 in 2025 from 3,790. Builders pulling back tells you what people closest to the money think

- Rates aren't going back to pandemic lows. BCREA forecasts 5-year fixed at 4.6% in 2026, 4.7% in 2027

- BC was the only province with negative population growth in Q2 2025. Fifth consecutive quarter of net non-permanent resident loss

- Alberta has been the #1 destination for interprovincial migration in Canada for 12 straight quarters

That's the honest list. None of it is fatal. Most of it is cyclical, not structural. But you should know what you're looking at.

What the data isn't telling you yet

Everything above is a lagging indicator. It tells you what already happened.

What I'm seeing in the last few weeks tells a different story. And I'll b honest— I don't have data to back this up yet. It's a hunch.

I'm getting more calls from Alberta and Vancouver than I've had in months. Not just inquiries. Real conversations from people seriously thinking about making a move. Some are Alberta buyers who got priced out of Calgary's runup. Some are Vancouver owners finally looking at the price gap and pulling the trigger on the lifestyle move they've been talking about for years.

It's anecdotal. It's a feeling. But sentiment moves before stats do. By the time the Q2 numbers come out and confirm what's happening, the window is already closing.

Stats Canada and BCREA will tell you what happened three months ago. The phone tells you what's about to happen.

What this actually means for you

If you're thinking about selling. You're not in a falling market. You're in a market with more competition than usual but with a buyer pool that's structurally healthier than the Lower Mainland. Pricing matters more than it did in 2021. So does presentation. The equity is there if the home is positioned properly.

If you're thinking about buying. Waiting for a Vancouver-style crash here isn't a strategy that's going to work. The owner base isn't going to capitulate. If sentiment is starting to turn — which my phone says it might be — the next six months might end up being one of the better windows we've had in two years.

If you're an investor looking at condos. The STR-eligible buildings are worth a serious second look. The June 1 opt-out changes the math. Get the address-level confirmation before you write an offer. Not every building qualifies and not every unit in a qualifying building is a buy.

If you're not sure where you stand. That's the conversation worth having. The right move right now depends on your situation, not on a market-wide narrative.

The bottom line

The Okanagan is in better shape than the headlines suggest, but worse shape than 2025 suggested.

We outperformed the rest of BC last year. That part is real. But early 2026 cooled off. Unemployment is up. People are leaving for Alberta. The condo segment is just starting to find its footing.

What's working in our favour is structural, not cyclical. A top-10-in-Canada mortgage-free owner base. A diversified three-city economy. A lifestyle market that brings buyers in for reasons that aren't purely financial. That foundation isn't going anywhere.

The condo segment may have finally found a floor with the STR rules clarifying. And while the data is lagging, the calls coming in suggest the sentiment may already be turning.

The honest answer is this — it's a balanced market with real tailwinds, real headwinds, and an early signal that the next leg might be moving sooner than the data is showing.

The right move depends entirely on the individual situation. Not on a market-wide narrative.

Let's talk

This market is not one-size-fits-all. If you’re thinking about buying, selling, investing, or just trying to plan your next move, call/text 778-946-6454 . I’m happy to give you an honest read on your situation.

Mark Coons Personal Real Estate Corporation Selling Okanagan Group | eXp Realty 778-946-6454 [email protected]